This article is featured in the fall edition of our 360 Insights Quarterly Client Newsletter.

This article is featured in the fall edition of our 360 Insights Quarterly Client Newsletter.

As we approach Election Day on November 8, there will be endless debate, prognostication and media hype. But even before a single vote has been cast, the potential results are already being priced into stocks around the world.

While elections do have real consequences and can certainly impact individual companies, in aggregate they tend to be less important than many of the other factors that drive stock prices.

How much influence will the next President have on the price of Apple’s phones and computers, Nike’s apparel, Disney’s entertainment or Starbucks coffee?

What matters more: who becomes president or whether a company’s product is any good?

Continue reading

Tag Archives: Client Ready

No One Knows What Will Happen with Brexit… But Long-Term Investors Probably Shouldn’t Worry Too Much

This blog is from the July issue of Portfolio Perspectives.

This blog is from the July issue of Portfolio Perspectives.

Unlike fans of horror movies, markets hate scary surprises.

On June 22, many markets, even betting parlors, were predicting that British voters would opt to stay in the European Union (the odds went as high as 80% for staying). On June 23, gamblers and markets were proven wrong and stocks fell precipitously around the world, plunging more than 5% in the U.S. in just two days.

Some of the doomsayers from January, when the S&P 500 Index sank more than 10% and then rebounded to positive territory again by the end of Q1, came out of the woodwork to predict new Brexit-related disasters. Even European Council President Donald Tusk said, “I fear that Brexit could be the beginning of the destruction of not only the EU but also of western political civilization in its entirety.” Continue reading

Why Are You Buying Gold?

Source: Siegel, Jeremy, Future for Investors (2005), With Updates to 2014 Data is from Jan. 1, 1802 – December 2014. Hypothetical value of $1 invested on January 1, 1802 and kept invested through Dec. 2014. Assumes reinvestment of income and no transaction costs or taxes. This is for illustrative purposes only and not indicative of any investment. Indexes are unmanaged baskets of securities that are not available for direct investment by investors. Index performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Stock investing involves risks, including volatility (up and down movement in the value of your assets) and loss of principal. Investors with time horizons of less than five years should consider minimizing or avoiding investing in common stocks. Bonds are subject to market and interest rate risk. Bond values will decline as interest rates rise, issuer’s creditworthiness declines, and are subject to availability and changes in price. The price of gold may be affected by global gold supply and demand, currency exchange rates and interest rates. Investors should be aware that there is no assurance that gold will maintain its long-term value in terms of purchasing power in the future. T Bills are backed by the US government and are subject to interest rate and inflation risk. T Bill values will decline as interest rates rise. The value of the U.S. dollar depreciates over time with inflation, so the primary risk is inflation risk.

This blog is from the September issue of Portfolio Perspectives.

I don’t know about you, but lately my newsfeed has been inundated with headlines and stories about gold. It seems many of these articles are written or sponsored by someone trying to get me to buy the shiny metal. Many make the same cliché claims about why gold is a wise investment: it provides safety during financial crises, it hedges against inflation and it creates wealth. Unfortunately, these claims encourage people to buy gold for the wrong reasons. Continue reading

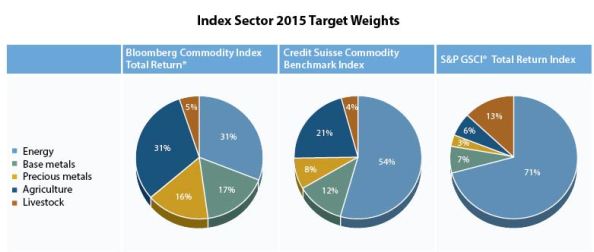

What did Commodities Return in 2014?

- Commodities as a whole were down in 2014 but depending upon which index you benchmarked to that loss may have been anywhere from -17% to -33%

- Commodity returns can vary widely depending on the underlying exposure to each sector

- This difference in sector makeup can cause profound differences in long-term results, but we won’t know in advance which methodology will perform the best

You must be logged in to post a comment.