What can skydiving teach us about investing? It teaches about risk and reward, and can give you a perspective on risk that may change the way you think about investing. Continue reading

Category Archives: Investing

Investing for the Future, Not in the Future

A version of this article appears in our spring 360 Insights quarterly newsletter.

A version of this article appears in our spring 360 Insights quarterly newsletter.

“I have no doubt that in reality the future will be vastly more surprising than anything I can imagine.”

– J. B. S. Haldane

In the 1967 movie, The Graduate, the young, newly minted college graduate is advised by a family friend that the future is about one word: “plastics.” The advice was a deliberately absurd laugh line, but in today’s era of unprecedented technical and societal change, we hear a great deal of similar advice delivered with perfect seriousness. Self-driving cars will change the world! We are on the cusp of revolutions in biotech, renewal energy, robotics, genetics, artificial intelligence, etc. Heck, we might even get flying cars and jet packs one day soon.

Any and all of these great changes might and probably even will happen and could very well revolutionize society, but things rarely work out quite as predicted — and even when they happen exactly as planned, trying to invest in the future is still a very, very risky thing to do.

Some investors believe they will make a fortune if they can only identify the companies that will create the revolutionary products and services of tomorrow. Others believe that established industry leaders such as Apple, Facebook, Google or Amazon will continue to grow, innovate and dominate their competitors and thereby reward investors with strong returns.

If only investing were so easy.

To demonstrate some of the perils in investing in the future, let’s consider a groundbreaking and prescient Time Magazine article published in April of 1965 on “The Computer in Society,” which detailed all the ways computers were changing the world.

According to the article, “As the most sophisticated and powerful of the tools devised by man, the computer has already affected whole areas of society, opening up vast new possibilities by its extraordinary feats of memory and calculation….It has given new horizons to the fields of science and medicine, changed the techniques of education and improved the efficiency of government. It has affected military strategy, increased human productivity, made many products less expensive and greatly lowered the barriers to knowledge.”

Time noted that IBM was then the leading global computer company, with 74% of the U.S. computer market, “a dominance that leads some to refer to the industry as ‘IBM and the Seven Dwarfs.’ The dwarfs, small only by comparison with giant IBM: Sperry Rand, RCA, Control Data, General Electric, NCR, Burroughs, Honeywell.”

But Time’s reporting was already behind the times, neglecting to mention a computer firm which would transform technology and computing and become one of the 20 largest companies in America as well as the grandfather of Silicon Valley. Founded in a garage in Menlo Park, CA, in 1947, Hewlett Packard (HP) would enter the computer market in 1966 with the HP 2116A minicomputer — one of the first portable and “plug and play” computers.

As a thought experiment, let’s say that you were convinced by the Time article that computers would change the world and called your stockbroker and invested $100 in IBM as well as in each of the Seven Dwarfs at the beginning of 1966. After all, you wouldn’t want to put all your money in just one stock. You’ve also heard something about HP, so you invest $100 in their stock, as well as $100 in the S&P 500 for a little more diversification. If you’d stayed invested for the next 50+ years through 2016, here’s how your investment in the future would have done…

Some winners, some losers, but overall not too bad. Looks like investing in the future was a pretty good idea, until you consider the top-performing stock of that same period — a company that makes a heavily regulated, low-tech product. If you had invested $100 in Phillip Morris/Altria, it would have grown to $549,087 by 2016. Who would have thought in 1966 (and certainly in 2017) that tobacco, not computers would win the future (at least in terms of returns).

Even if you had known in 1966 everything that would happen in the world (except stock prices) over the next five decades, do you think you would have invested in tobacco stocks not tech? Like many of the realities of the stock market, it makes no intuitive sense.

Some of the other top-performing stocks over this period were also surprisingly non-innovative and low tech. For example, Coca Cola returned $34,403 and its cola rival Pepsico returned $21,084, better than any of the tech companies that would change the future.i

Or in the shorter-term, let’s look at the summer of 2004 when two firms went public, Google and Domino’s Pizza. One of these is a leading tech firm that revolutionized internet search, mapping, email and possibly, driverless cars. The other makes less than gourmet pizza. Most rational investors given the choice between the two firms would naturally assume that Google was the better investment. And they certainly did well over this period, returning 1,555% through January 14 2017. But Domino’s delivered a cumulative 2,401% return.

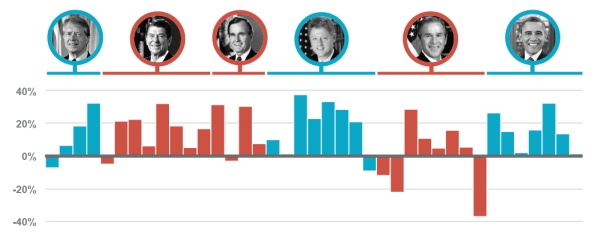

Or consider the top performing stocks of the Obama administration. While some, such as Netflix and Priceline were indeed innovators, the best performer was a chain of salons/beauty stores best known for their discounts, ULTA Salon, which returned 4,350%.1

Why should this be the case? What are some of the risks in investing in innovation?

Many times, innovative companies fall victim to second mover advantage as other firms build on and enhance the original technology. Think of how social media platforms like My Space were superseded by Facebook or smartphone makers like Blackberry were outmoded by Apple’s iPhone. It is hard to know whether a company will be a failed leader or a successful follower.

Also, the initial results of innovation can be hard to maintain. Think of once great firms such as Wang Computers or Nokia or Kodak (the inventor of the digital camera) that could not keep up and fell by the wayside. By market capitalization, Apple is the largest company in the world. Millions of people use — and love — their products. But will they still be a tech leader 10 years from now? 20?

Newer industries often deliver disappointing returns when investors turn out to be too optimistic about the potential for future growth. As Professor Jeremy Siegel, an authority on long-term investing, notes: “Investors have a propensity to overpay for the ‘new’ while ignoring the ‘old’ … growth is so avidly sought after that it lures investors into overpriced stocks in changing and competitive industries, where the few big winners cannot compensate for the myriad of losers.”2

In comparison to growth stocks, which are very often innovative, forward-looking companies with strong earnings growth (or potential growth), value stocks are usually associated with generally less-innovative corporations that have experienced slower earnings growth or sales, or have recently experienced business difficulties, causing their stock prices to fall. Academic research has shown however that value company stocks have greater expected returns — and greater risk — than growth company stocks. Since 1927, U.S. Large Value stocks have returned 10.51% vs 9.43%3 for U.S. Large Growth stocks. This makes sense, since riskier companies must offer a higher potential return to attract investors.

In addition, old industries often continue to be surprisingly profitable. Consider the U.S. transportation index. From 1900 – 2015, railroads were the top performers, beating airlines, road transport (which joined the index in 1926) and the U.S. market, while airlines (which joined the index in 1934) trailed the market substantially.4 As Warren Buffet said about the Wright Brothers, “If a farsighted capitalist had been present at Kitty Hawk, he would have done his successors a huge favor by shooting Orville down.”

The future may be uncertain, and the great companies of tomorrow may not always be the best investments. But the future, taken as a whole, may be the best investment many of us make.

If we are prepared to take a patient, long-term perspective and buy and hold securities from thousands of great companies around the world, we may benefit from two powerful forces:

- Compounding, which allows your money to grow exponentially over time. If your portfolio grows an average of 6%, for example, it will double every twelve years. In 48 years, $100,000 growing at this rate becomes $1.6 million.

- The dynamic potential of stock markets, fueled by human innovation, to create enduring wealth over time.

We don’t know which firms will be the next Domino’s or Google. We don’t know which firms will soar and which will fail, which will invent amazing new products and which will make money by doing what they have always done. But if we own many of them and invest for the future, chances are we will be rewarded over the long term.

All investing involves risk. Principal loss is possible. Past performance does not guarantee future results.

Diversification neither assures a profit nor guarantees against loss in a declining market.

iSource: Yahoo Finance

1The Motley Fool, “The 10 Best Stocks During the Obama Administration,” January 19, 2017

2Siegel, Jeremy, 2005, The Future for Investors: Why the Tried and the True Triumph over the Bold and the New, New York, NY: Crown Publishing Group.

3DFA Returns 2.0. Fama/French US Large Value ex Utilities and Fama/French US Large Growth ex Utilities

4Credit Suisse Global Investment Returns Yearbook – 2015

17-094

The Lesson of $1

Hypothetical value of $1 invested at the beginning of 1927 and kept invested through December 31, 2016. Assumes reinvestment of income and no transaction costs or taxes. This is for illustrative purposes only and not indicative of any investment. Total returns in U.S. dollars. Past performance is no guarantee of future results.

U.S. Stock Market represented by the Fama/French Total US Market Index Portfolio, which is an an unmanaged index of stocks representing stocks of U.S. companies. U.S. Small Cap Stocks represented by the Fama/French US Small Cap Index, which is an unmanaged index of stocks of small U.S. companies. U.S. Value Stocks represented by Fama/French US Large Value Index (ex utilities), which is an unmanaged index of stocks of large U.S. companies with low relative price, excluding utilities companies. The Consumer Price Indexes (CPI) program produces monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services. Long-Term Government Bonds, One-Month U.S. Treasury Bills, and U.S. Consumer Price Index (inflation), source: Morningstar’s 2016 Stocks, Bonds, Bills, And Inflation Yearbook (2016). Indexes are unmanaged baskets of securities that investors cannot directly invest in. Index performance does not reflect the fees or expenses associated with the management of an actual portfolio.

The risks associated with investing in stocks and overweighting small company and value stocks potentially include increased volatility (up and down movement in the value of your assets) and loss of principal. Bonds are subject to market and interest rate risk. Bond values will decline as interest rates rise, issuer’s creditworthiness declines, and are subject to availability and changes in price. T Bills and government bonds are backed by the U. S. government and guaranteed as to the timely payment of principal and interest. T Bills and government bonds are subject to interest rate and inflation risk and their values will decline as interest rates rise. The Consumer Price Indexes (CPI) program produces monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services.

Hypothetical value of $1 invested at the beginning of 1927 and kept invested through December 31, 2016. Assumes reinvestment of income and no transaction costs or taxes. This is for illustrative purposes only and not indicative of any investment. Total returns in U.S. dollars. Past performance is no guarantee of future results.

U.S. Stock Market represented by the Fama/French Total US Market Index Portfolio, which is an an unmanaged index of stocks representing stocks of U.S. companies. U.S. Small Cap Stocks represented by the Fama/French US Small Cap Index, which is an unmanaged index of stocks of small U.S. companies. U.S. Value Stocks represented by Fama/French US Large Value Index (ex utilities), which is an unmanaged index of stocks of large U.S. companies with low relative price, excluding utilities companies. The Consumer Price Indexes (CPI) program produces monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services. Long-Term Government Bonds, One-Month U.S. Treasury Bills, and U.S. Consumer Price Index (inflation), source: Morningstar’s 2016 Stocks, Bonds, Bills, And Inflation Yearbook (2016). Indexes are unmanaged baskets of securities that investors cannot directly invest in. Index performance does not reflect the fees or expenses associated with the management of an actual portfolio.

The risks associated with investing in stocks and overweighting small company and value stocks potentially include increased volatility (up and down movement in the value of your assets) and loss of principal. Bonds are subject to market and interest rate risk. Bond values will decline as interest rates rise, issuer’s creditworthiness declines, and are subject to availability and changes in price. T Bills and government bonds are backed by the U. S. government and guaranteed as to the timely payment of principal and interest. T Bills and government bonds are subject to interest rate and inflation risk and their values will decline as interest rates rise. The Consumer Price Indexes (CPI) program produces monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services.

[/caption]One of the best opportunities to grow your money over the long term may come from making an investment in the stock market.

This chart illustrates the long-term growth of U.S. businesses over the past 90 years. If your grandparents had invested $1 in the U.S. Stock market, as measured by the Fama/French Total US Market Index, in 1927 and just left it alone, by the end of 2016 that $1 would have grown to $5,106. Invested in U.S. Small Cap Stocks, as measured by the Fama/French US Small Cap Index, that $1 would have grown to $24,586, and $8,050 if invested in U.S. Value Stocks, as measured by the Fama/French US Large Value Index. That same $1 invested in One-Month T-Bills would be worth $20 and if invested in Long- Term Government Bonds it would be worth $125.

Those who invested $1 back in 1927 would have had plenty of reasons to want to pull out of the market along the way — The Great Depression, World War II, Korea, Viet Nam, stagflation, the Great Recession — but by staying invested they could take advantage of every market recovery.

While we can never be certain about market direction in the short term, over the long-term we believe patient investors will be rewarded for staying invested.

17-076

6 Ways We’ve Just Enhanced Loring Ward’s Blog

In January of 2014 we introduced our Advisor Insights Blog with the goal of providing financial advisors and their clients with timely and timeless financial education and insights.

In January of 2014 we introduced our Advisor Insights Blog with the goal of providing financial advisors and their clients with timely and timeless financial education and insights.

Since then, we’ve published more than 200 articles — with 85,000+ views — on a wide variety of topics, from Asset Class investing to financial planning, retirement, behavioral finance, practice management and marketing. We’ve even included a few recipes from employees along the way.

Continue reading

Happy Pi Day (Cherry Pie Included)!

In case you are feeling short of things to celebrate, there is always Pi Day – March 14 (3/14).

In case you are feeling short of things to celebrate, there is always Pi Day – March 14 (3/14).

As you remember from high school math, Pi (Greek letter “π”) is a mathematical symbol representing the ratio of a circle’s circumference to its diameter — which is approximately 3.14159.

Continue reading

Why Uncertainty Might Just Be an Investor’s Best Friend

This blog is from the March issue of Portfolio Perspectives.

This blog is from the March issue of Portfolio Perspectives.

With many stock market indices at all-time highs, Washington awash in political turmoil and unsettling news around the globe, many investors may be unsure what to do next.

And we believe that is a good thing.

Continue reading

3 Reasons Investors Should Update Their Investment Policy Statement

Just as regular health checkups with a qualified physician are an important proactive step to maintaining your physical health, regular financial checkups with an experienced financial advisor are an important proactive step to maintaining good financial health.

Just as regular health checkups with a qualified physician are an important proactive step to maintaining your physical health, regular financial checkups with an experienced financial advisor are an important proactive step to maintaining good financial health.

Continue reading

The Future Isn’t What It Used to Be — The Great Predictive Failures of 2016

This article is featured in the winter edition of our 360 Insights Quarterly Client Newsletter.

This article is featured in the winter edition of our 360 Insights Quarterly Client Newsletter.

The New York Post headline the day after the 2016 U.S. elections put it best: “Pundits, Polls, Politicians, the Press: EVERYONE WAS WRONG.”

From the U.S. elections to Brexit to economic doomsaying, 2016 saw a series of spectacularly erroneous predictions. Again and again, experts were proven wrong and had to scramble to explain why they had missed the mark so badly. Continue reading

2016: The Most Typical Year Nobody Saw Coming

“It’s the 2008 Crisis all over again,” “Prepare for stocks to fall another 10%,” “World Economy Trapped in a ‘Death Spiral,’ ” “Sell Everything”1 — these were the loudest sentiments we heard from prominent industry participants in the first few weeks of 2016. Yet, as we close the books on another year’s positive gain, we’re reminded that stock market rallies don’t die of old age or pundit predictions. With the S&P 500 advancing 11.96%, we’ve now seen a cumulative gain of over 280% since the lows of 2009.

“It’s the 2008 Crisis all over again,” “Prepare for stocks to fall another 10%,” “World Economy Trapped in a ‘Death Spiral,’ ” “Sell Everything”1 — these were the loudest sentiments we heard from prominent industry participants in the first few weeks of 2016. Yet, as we close the books on another year’s positive gain, we’re reminded that stock market rallies don’t die of old age or pundit predictions. With the S&P 500 advancing 11.96%, we’ve now seen a cumulative gain of over 280% since the lows of 2009.

Continue reading

What Happened Last Quarter… and Why Does it Matter?

Source: Chart sourced from How The Election Will Really Affect Your Investments, Money magazine, June 22, 2016. Returns from Morningstar Direct 2016 returns represent S&P 500 annual total return. Indexes are unmanaged baskets of securities that are not available for direct investment by investors. Index performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. All investments involve risk, including the loss of principal and cannot be guaranteed against loss by a bank, custodian, or any other financial institution.

- Performance: Remember the Royal Bank of Scotland’s decree to “sell everything” earlier this year? Hopefully you didn’t pay attention to it, as gains continued in Q3; only U.S. REITs declined marginally in value. The big reversal was solid gains from Emerging Markets Value, International Small Cap and International Value, which all outpaced the S&P 500.

How to Lose Money

This blog is from the October issue of Portfolio Perspectives.

This blog is from the October issue of Portfolio Perspectives.

Loring Ward recently honored Dr. Harry Markowitz with our Heritage Award for his contributions to financial science that have impacted millions of investors as well as his many years of service on our Investment Committee. In recognition, we would like to share some insights from Dr. Markowitz adapted from his afterword to our book on wealth management: “The Wealth Solution.”

If you want to become an acknowledged Saint, it is best if you start by giving away all your money. If this prospect sounds too daunting, the following are four efficient suggestions for reducing your wealth. The first two may only lose most of it but the final two will make it all disappear. Continue reading

Do All-Time Highs Mean Overvalued Markets?

Stock Market Performance in the Periods Following All-Time Record Highs

This is the second in a two-part blog of our Quarterly Investment Committee Briefing.

This is the second in a two-part blog of our Quarterly Investment Committee Briefing.

On August 15, several of the major U.S. stock market indices reached all-time high levels. The Dow Jones Industrial Average, the S&P 500 and the Russell 3000 all closed at record highs, welcome news for the average stock investor who has patiently invested for the long-term.

But many ask, “Does the fact that a stock market index breaks through to an all-time high suggest that the market is at a precarious level?” It can be tempting to compare a stock market at its all-time high to standing on top of a tall mountain — it’s a lofty height with nowhere to go but down. But is this an accurate analogy? Continue reading

Q3 Investment Committee Briefing

This is the first in a two-part blog of our Quarterly Investment Committee Briefing.

This is the first in a two-part blog of our Quarterly Investment Committee Briefing.

So far this year, one of the big stories in global markets was the surprise Brexit vote in the third week of June. Conventional wisdom was that this event was a harbinger of future economic weakness and lower markets. Markets fell a bit on the news; however, as so often happens with conventional wisdom, it was quickly cast aside. By the start of Q3, the S&P 500 had almost recovered to its 2016 high levels. In the weeks that followed, the S&P 500 and several other major stock indexes crept higher… until August 15 when they broke through to an all-time record high level. Continue reading

Dr. Harry Markowitz Honored by Loring Ward

Loring Ward today awarded Dr. Harry Markowitz its Heritage Award at the firm’s National Education Conference in San Diego. Markowitz, best known for winning the Nobel Prize in Economic Sciences in 1990 for his work on portfolio selection, has served on Loring Ward’s Investment Committee since 2010.

Loring Ward today awarded Dr. Harry Markowitz its Heritage Award at the firm’s National Education Conference in San Diego. Markowitz, best known for winning the Nobel Prize in Economic Sciences in 1990 for his work on portfolio selection, has served on Loring Ward’s Investment Committee since 2010.

According to Loring Ward’s CEO, Alex Potts, “Our firm has drawn on the research and powerful insights of many leading academics to build our Asset Class Investing portfolios, but no one has had a larger and more wide ranging impact than Dr. Markowitz. We are so privileged to be able to honor his lifetime of contributions to financial services, and to recognize his impact on millions of investors.”

Continue reading

Flip a Coin and Learn About Your Portfolio

This blog is from the August issue of Portfolio Perspectives.

This blog is from the August issue of Portfolio Perspectives.

Even if you don’t consider yourself much of a gambler, you probably can answer this question correctly: Are you likely to lose more money placing one $100 bet or 50 $2 bets?

If you answered the $100 bet you are right, but what does this have to do with investing?

Imagine that we flip a coin. If it comes up heads, I’ll pay you $2; if it comes up tails, you’ll pay me $1. We can play this game in any relative amount and we can flip the coin as many times in a row as you want. You have a 50% chance of receiving $2 and a 50% chance of having to pay $1. Therefore, your “expected value” on such a game would be 50 cents on each flip for every $1 you are willing to put at risk. Continue reading

Keep Your Eye on Your Goals

If someone asked you, “Why is wealth important to you?” what would be your answer? In a survey of high-net-worth families, financial security was the most popular answer, followed by help children become successful, educate children and help the less fortunate.1

If someone asked you, “Why is wealth important to you?” what would be your answer? In a survey of high-net-worth families, financial security was the most popular answer, followed by help children become successful, educate children and help the less fortunate.1

Financial security is more than money in our portfolios; it is the confidence that we can continue to live in dignity and support ourselves financially rather than rely on our children.

A diversified portfolio that follows our Investment Policy Statement is most likely to get us to our long-term goals — like financial security and helping our children — yet we worry daily as we watch markets go up and down. Continue reading

WHY Global Stock Markets May be the Greatest Creators of Wealth We Have Ever Known

I cringe whenever I hear someone say that they’re, “playing the stock market.” The stock market is not a competitive game, with winners and losers. Instead, it offers the potential for every investor with a globally diversified portfolio and a long-term perspective to win. Here’s why:

I cringe whenever I hear someone say that they’re, “playing the stock market.” The stock market is not a competitive game, with winners and losers. Instead, it offers the potential for every investor with a globally diversified portfolio and a long-term perspective to win. Here’s why:

If you’re “playing” you’re probably doing a lot of buying and selling based on what stocks you think will underperform or outperform. But we know from history and extensive research1 that almost no one — not even the smartest and best-educated among us — can consistently and accurately predict which stocks will be winners or losers, or when the market will go up or down.

If you’re playing the stock market, you’re thinking and worrying all the time about whether the “winners” you’ve picked are actually “winning.” Should you buy more? Should you sell? Continue reading

Main Street vs. Wall Street — Why Investing is NOT Speculating

I was talking with an experienced Advisor and he said that many of his clients are concerned that the financial system is rigged against them — constructed by policy makers, regulators, banks, rating agencies and Wall Street firms for their own benefit.

I was talking with an experienced Advisor and he said that many of his clients are concerned that the financial system is rigged against them — constructed by policy makers, regulators, banks, rating agencies and Wall Street firms for their own benefit.

“Clients feel sometimes as if they are playing in a casino, where the house always wins,” the Advisor said. “How do I help them understand the difference between Wall Street and what I do?”

This question made me reflect on how poorly served we are by Wall Street as a whole, as well as the financial media. All the hype and noise and product pushing serve only to obscure some very simple and powerful truths. Continue reading

No One Knows What Will Happen with Brexit… But Long-Term Investors Probably Shouldn’t Worry Too Much

This blog is from the July issue of Portfolio Perspectives.

This blog is from the July issue of Portfolio Perspectives.

Unlike fans of horror movies, markets hate scary surprises.

On June 22, many markets, even betting parlors, were predicting that British voters would opt to stay in the European Union (the odds went as high as 80% for staying). On June 23, gamblers and markets were proven wrong and stocks fell precipitously around the world, plunging more than 5% in the U.S. in just two days.

Some of the doomsayers from January, when the S&P 500 Index sank more than 10% and then rebounded to positive territory again by the end of Q1, came out of the woodwork to predict new Brexit-related disasters. Even European Council President Donald Tusk said, “I fear that Brexit could be the beginning of the destruction of not only the EU but also of western political civilization in its entirety.” Continue reading

4 Ways to Help Manage Risks

Source: Dimensional. In U.S. dollars. Market cap data is free-float adjusted from Bloomberg securities data. Many small nations not displayed. Totals may not equal 100% due to rounding. Past Performance is not indicative of future results. All investments involve risk. Foreign securities involve additional risks including foreign currency changes, taxes and different accounting and financial reporting methods. Countries represented by their respective MSCI IMI(net div.). Indexes are unmanaged baskets of securities in which investors cannot directly invest; they do not reflect the payment of advisory fees or other expenses associated with specific investments or the management of an actual portfolio.

This is the third article of a four-part series to help you understand our investment approach — and why it matters to you.

Look up the word RISK in a thesaurus and you see words like danger and hazard, but also opportunity and fortune. Continue reading

You must be logged in to post a comment.